Essay·Averin Capital

When Biotech Crowds Into Consensus, the Real Returns Begin Elsewhere

Jeffrey Low, MDDecember 17, 2025

Originally published on Averin Capital →The biotech industry is increasingly optimized for consensus safety at the precise moment when the next generation of outsized returns is being seeded elsewhere. Across boardrooms and investment committees, the same preferences keep surfacing:

- Later-stage assets over foundational science

- Validated targets and modalities over new biology

- Pipelines over platforms

- Even historically early investors drifting later under fund-cycle pressure

This shift is rational. In uncertain markets, consensus feels prudent.

But it creates a structural mismatch: the biology that will matter in 2030 and beyond has to be started now.

New modalities and mechanisms do not mature on a one-year timeline. They require years of iteration, validation, and operational de-risking. When markets inevitably swing back to reward innovation, the supply of truly novel companies will be thin. Scarcity, as always, drives asymmetric outcomes.

We have seen this dynamic before.

The last time capital pulled back

Following the financial crisis of 2008, much of the venture capital industry retreated toward safer, more legible bets. Yet a small set of firms leaned into innovation rather than away from it, backing companies founded roughly between 2008 and 2012 that looked like dead ends to the prevailing consensus.

At the time:

- Gene therapy was considered too dangerous

- mRNA was viewed as unstable and impractical

- Cardiovascular drug development was being abandoned by large pharma

- Kinase inhibitors were dismissed as "dirty" and commoditized

This cohort, formed during a period of capital scarcity and deep skepticism toward long-cycle biology, ignored the consensus and ultimately generated tens of billions of dollars in enterprise value.

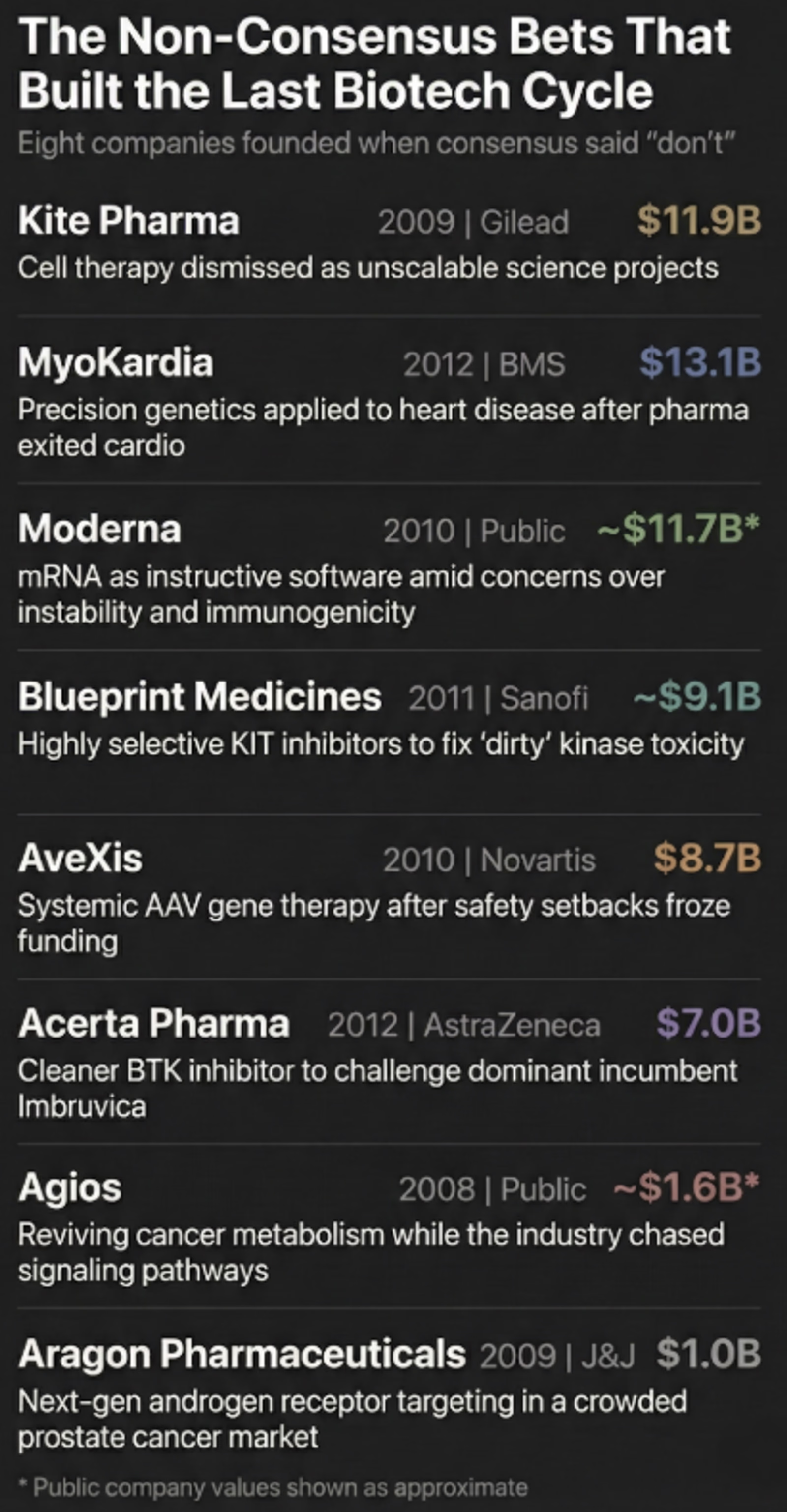

Below are eight illustrative examples of how non-consensus builds went on to define the last great biotech cycle.

1. The "Science Projects"

Betting on new modalities when feasibility was doubted

The consensus view was that these technologies were too early, too risky, or physically impossible to turn into real medicines.

Kite Pharma (Founded 2009)

- The consensus: Cell therapy is a bespoke academic experiment. It cannot be manufactured or scaled.

- The bet: Engineered T cells could induce durable remissions in hematologic cancers.

- The result: Acquired by Gilead for $11.9B.

AveXis (Founded 2010)

- The consensus: Gene therapy is dead. Systemic delivery is unsafe and unworkable.

- The bet: High-dose AAV9 could safely replace missing genes in infants with spinal muscular atrophy.

- The result: Acquired by Novartis for $8.7B.

Moderna (Founded 2010)

- The consensus: mRNA is too unstable and immunogenic to function as a drug.

- The bet: mRNA could act as instructive software, enabling the body to manufacture its own therapeutics.

- The result: Peaked at over $200B in market capitalization and remains an independent public company.

2. The "Abandoned Spaces"

Reviving biology others had written off

The consensus view was that these therapeutic areas were graveyards where pharma capital went to die.

MyoKardia (Founded 2012)

- The consensus: Cardiovascular drugs are a bad investment. Trials are expensive and failure rates are high.

- The bet: Precision genetics could be applied to hypertrophic cardiomyopathy just as it had been in oncology.

- The result: Acquired by Bristol Myers Squibb for $13.1B.

Agios Pharmaceuticals (Founded 2008)

- The consensus: Cancer metabolism is elegant academic biology with limited clinical relevance.

- The bet: Targeting metabolic enzymes such as IDH could represent a third pillar of oncology alongside signaling and immunotherapy.

- The result: Created substantial value through the sale of its oncology business and the emergence of a standalone rare disease franchise.

3. The "Precision Scalpels"

Selectivity as a durable moat

The consensus view was that these markets were already won by incumbents or that the chemistry challenges were unsolvable.

Blueprint Medicines (Founded 2011)

- The consensus: Kinase inhibitors are commoditized and inherently toxic.

- The bet: Highly selective, mutation-specific inhibitors could deliver transformative benefit in genomically defined diseases such as systemic mastocytosis.

- The result: Acquired by Sanofi in 2025 for approximately $9.1B.

Acerta Pharma (Founded 2012)

- The consensus: Imbruvica owns the BTK market. There is no room for a second player.

- The bet: A cleaner, more selective BTK inhibitor could outperform a dominant incumbent.

- The result: Acquired by AstraZeneca for approximately $7.0B.

Aragon Pharmaceuticals (Founded 2009)

- The consensus: Prostate cancer is crowded and next-generation hormone therapies offer limited upside.

- The bet: Novel approaches to androgen receptor biology could overcome resistance and reset the field.

- The result: Acquired by Johnson & Johnson for approximately $650M upfront plus milestones, helping seed the protein degradation ecosystem that followed.

The lesson for the next cycle

These were not consensus trades. They were bold company builds executed when conviction was scarce.

Consensus deals will always have a place when validated biology meets excellent execution. But the generational outcomes in each cycle tend to come from the non-consensus builds that begin years earlier, when timelines are long and certainty is low.

The common thread across these companies is not simply that they succeeded. It is that they began by asking, "What is the market wrong about?" The alpha was not embedded in a single asset. It was embedded in a willingness to diverge from the crowd.

As we look at today's "uninvestable" spaces, whether complex CNS, longevity biology, or novel delivery technologies, it is worth remembering that the biggest returns often come from ideas that look most like science projects at the start.